By Kamil Knap, Ryan Sester

CHAPTER I. FINTECH

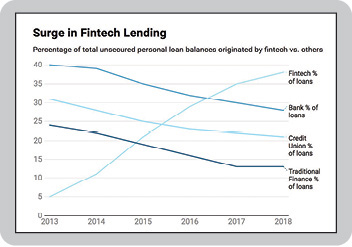

FinTech lending originated and has become popular in the United States and around the world in the 12 years since the 2008 financial crisis. FinTech innovators saw a need when larger banks reduced consumer lending and filled the void to provide financing. One of the main reasons behind the success is the digital setup of the marketing, underwriting and funding processes. The critical point of the online lending concept is to attract as many consumers and small to medium-sized businesses as possible by campaigns over the internet, social media, and emails. Utilizing the main advantage of lending — a product everybody wants — money helped to attract demand combined with a technology-based, online culture. In many cases, the campaigns are not focused on the loan itself but rather focused on the new utility or product that is now closer to the borrower through the loan. Each and every campaign is measured by utilizing different funnels, matrixes. The analysis of the lending process is optimized over different channels add more and more visitors to the webpage. Fintech has always been prepared to pay for that Facebook click and credit reporting lead.

Fintech’s initial focus is to attract as many visitors to the webpage as possible, having led 1000s of views and direct borrowers directly to the application. Potential and current borrowers are not shown a fancy company webpage or complex information. The objective is to make the click to an application as simple as possible.

For banks that operate in different parts of the country, what happens on the West Coast matters. So, what other public policy issues under discussion in California might spread? Last year, the governor signed a measure allowing municipalities to establish a public bank under the false narrative that private sector banks were misaligned with the value of their communities. We know that public banking advocates will take their success in California and attempt to export it to other states.

This January, Governor Gavin Newsom unveiled plans to restructure the regulatory agency that oversees California state-chartered financial institutions. Under the plan, the California Department of Business Oversight (DBO) will be renamed as the Department of Financial Protection and Innovation (DFPI) and will increase its emphasis on consumer protection and innovation relative to financial technology and products. These reforms are being advanced, in part, given concerns about a shift in priorities at the federal level, a desire for the state to demonstrate ongoing leadership, and an interest in fostering innovation and establishing the appropriate controls for providers of financial services.

According to preliminary information provided by the DBO, the purpose of this proposal is to 1) restore financial protections that have been paralyzed at the federal level; 2) protect consumers from predatory businesses, without imposing undue burdens on honest and fair operators; 3) spur — not stifle — innovation in financial services by clarifying regulatory expectations for emerging products and services; 4) extend state oversight to important financial-services providers not currently subject to state supervision; 5) increase public outreach and education, especially for vulnerable populations; and 6) provide more effective response to consumer complaints.

Should the plan to restructure DBO be successful, we anticipate other states will follow. California relishes and takes great pride in its role as a legislative pioneer. As the legislative year in California unfolds, we’ll have a better sense of public policy issues that may catch fire elsewhere.

CHAPTER II. APPLICATION

The application process on the Fintech Lender’s webpage is again optimized. What information do we need to know first, save the data, and then have the consumer proceed to the next page? Attract consumers to the amount of money they may apply for at an attractive rate, obtain the name, phone number, email and click next. Once the borrower does not continue the application, he may be contacted and asked if he needs assistance. This technology needs to be optimized and improved to facilitate the progression of the lender.

CHAPTER III. UNDERWRITING AND VERIFICATION

The Underwriting process is the next step. Underwriting starts with gathering the data required to evaluate risk and to make a sound decision. Engaging the borrower to be attracted to the process and motivated to move to the next step is critical. It is important to simultaneously make the process interesting to the consumer and to verify the details provided on the application are correct. Verification may be completed internally or by an external provider. Examples of fraud prevention analytics measure the time to enter a birthdate, how many times the name has been rewritten, asking the borrower to connect their bank account and additional information. In addition, complete a review to ensure the borrower is not stacking loans (other Fintech lenders providing loans to the same borrower concurrently.)

CHAPTER IV. NUMBERS

The Underwriting process had always been a challenge for Fintech lenders. Non-performing loans and the definition of NPL is not 100% aligned with best practices in the banking industry. Sometimes Fintech is viewed as more Tech (technology) than Fin (finance). One reason for this is attracting consumers with proper marketing and technology to apply for loans. Build the book if you will, and initially focusing on the process before risk. The concept of quick, reasonably priced processes with employees motivated by technology, relaxed culture and measurable criteria allowed the companies to attract a lot of interest from investors. Lenders considered this relatively low cost to obtain a loan as costs incurred with creating innovative technology to approve loans and retaining a performing part of the portfolio within the Fintech lender.

One of the factors by FinTech lenders that influenced their performance has been rollover from DPD 5 (5 days overdue) to DPD 30, then DPD 30 to DPD 60, DPD 60 to DPD 90, DPD 90 to 180 and charge-off. The charge-off ratio did not, initially, impact the lender’s valuation. In the growth stage, they calculated the number of loans getting to charge-off in comparison to the entire loan book. As lenders reached the stratosphere of maximum market penetration, the actual charge-off % did start to show. As many of the loans are not collateralized, the value of collateral did not allow to decrease the value of LGD. EAD (exposure at default) has dramatically increased as well, due to collection processes being impacted both internally and externally. A lack of resources, appetite and experience handling of collection accounts led to increases in delinquent accounts. Bad data entry, setup of legal agreements and lack of desire to pursue a judgment limited success on recovering principal on defaulted loans. Many judgments, if obtained, had been on a default judgment basis in the state of the legal department of the Fintech lender to both decrease costs and presumably to initiate payment discussions. Filing all judgments in the state of the lender would result in limited enforcement options of the judgments.

FinTechs also encounter different modes of fraud. If the fraud is occurring due to an invalid or third party SSN, the fraud is likely happening by repeat professional borrowers, or a borrower with no intention to repay the loan. Loans have been provided to borrowers to finance bankruptcy; loans without requiring an SSN or loans to small business, such as restaurants, have added additional risk to the business.

On the side of the revenue, FinTech is less regulated than a bank or credit union. One extreme example is a Title Loan company. They have the ability to receive revenue from the purchase, underwriting costs, servicing fees and ability to refer new services to clients to supplement the non-performing loan book.

Additionally, the constant change of Chief Risk Officers (usually every two years), different interests of boards in disagreements with investors over performance, and vision and pre-IPO valuation linked to the loan book had been a challenge.

2020 IIQ CHAPTER V

The second quarter of 2020 was the most challenging quarter in FinTech lenders’ lifecycles so far. There had been no financial crisis since 2008, and all the models will show the performance only in a good economic market. Publicly traded companies did publish financial numbers of Q1 2020 around April/May 2020. There was numerous information reported to read, comprehend, and draw conclusions from. The amount of loans being on work-out and the amount of loans not paying were daunting for a partial quarter impacted by COVID-19. Technical analysts at many equity trading platforms as Yahoo! Finance and others did not fully understand what was happening and recommendations to hold or buy seemed out of place, even at the time. Fundamentals did change.

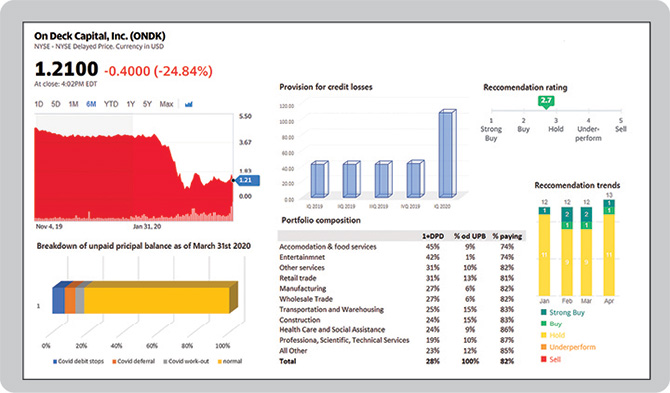

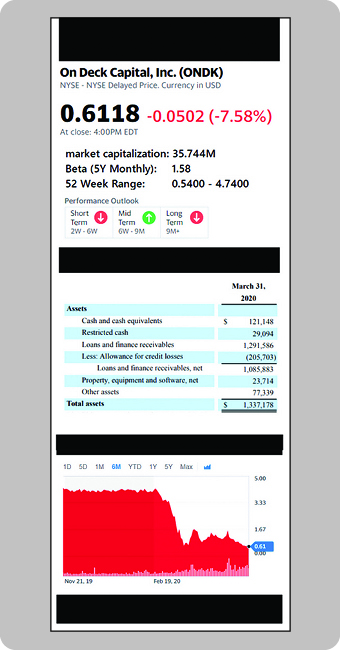

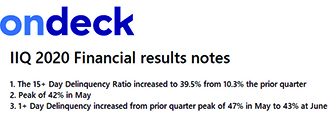

OnDeck results of IIQ 2020

In the end, the final selling price of OnDeck was $90 million, $8 million of which was paid in cash, with the remainder paid in Enova stock.

A very similar company to OnDeck named Kabbage (in terms of portfolio size) had been sold for around 800 million USD without the portfolio.

Name: Kamil Knap

Position: president and director

Company: EPA USA Inc.

Education: Stanford University,

City University of Hong Kong,

Masaryk University

Name: Ryan Sester

Position: CEO

Education: Arizona State University

This story appears in Issue 3 2020 of The Arizona Banker Magazine.